A Complete Breakdown of the Complex World of Global KYC

A Complete Breakdown of the Complex World of Global KYC

A Complete Breakdown of the Complex World of Global KYC

Navigating the complexities of international Know Your Customer (KYC) regulations is a significant challenge for businesses operating across borders. The.

Author

Product Marketing

Team Bureau

See how Bureau has helped industry leaders defend against networked Industrial-scale frauds →

Schedule a Demo

TABLE OF CONTENTS

See Less

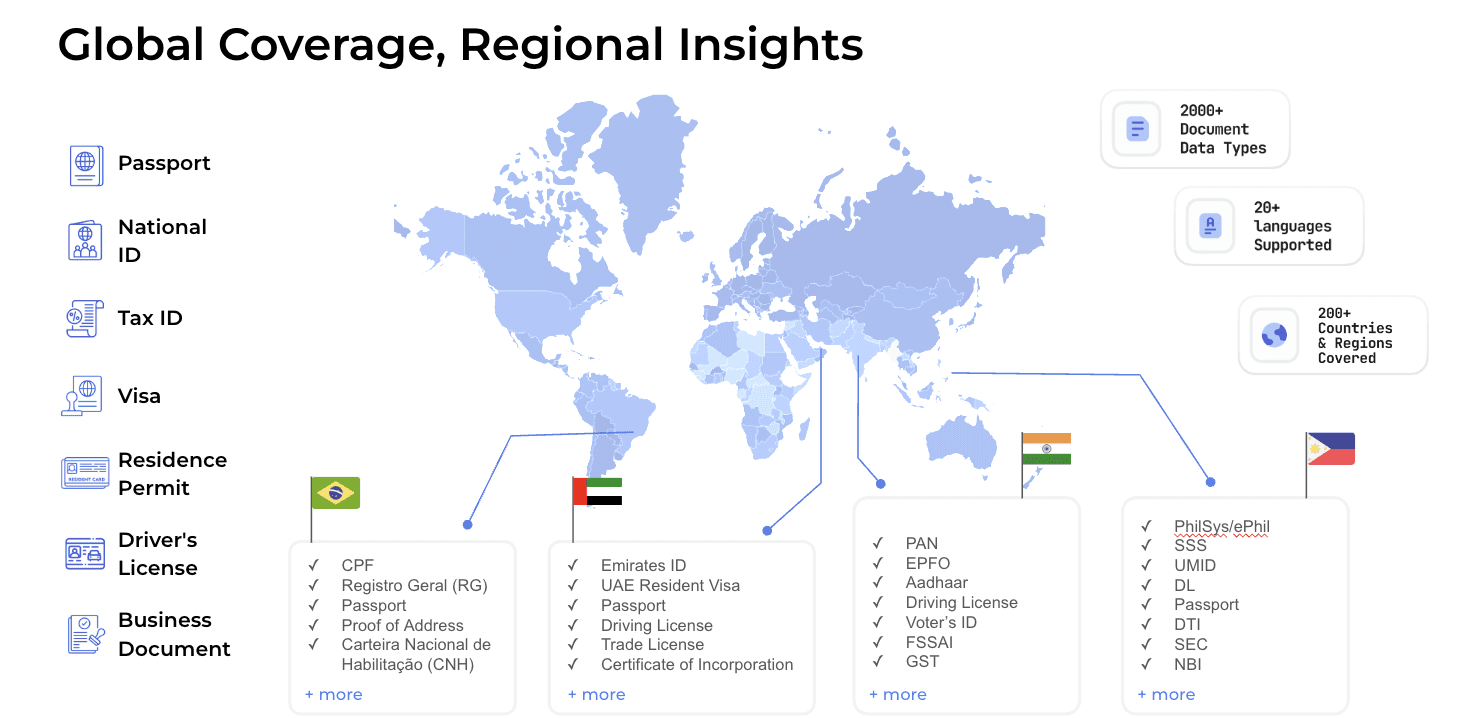

With a KYC stack that supports 2,000+ document types in 190+ countries, Bureau’s unified risk decisioning platform helps businesses maintain compliance with local, regional, and global KYC requirements

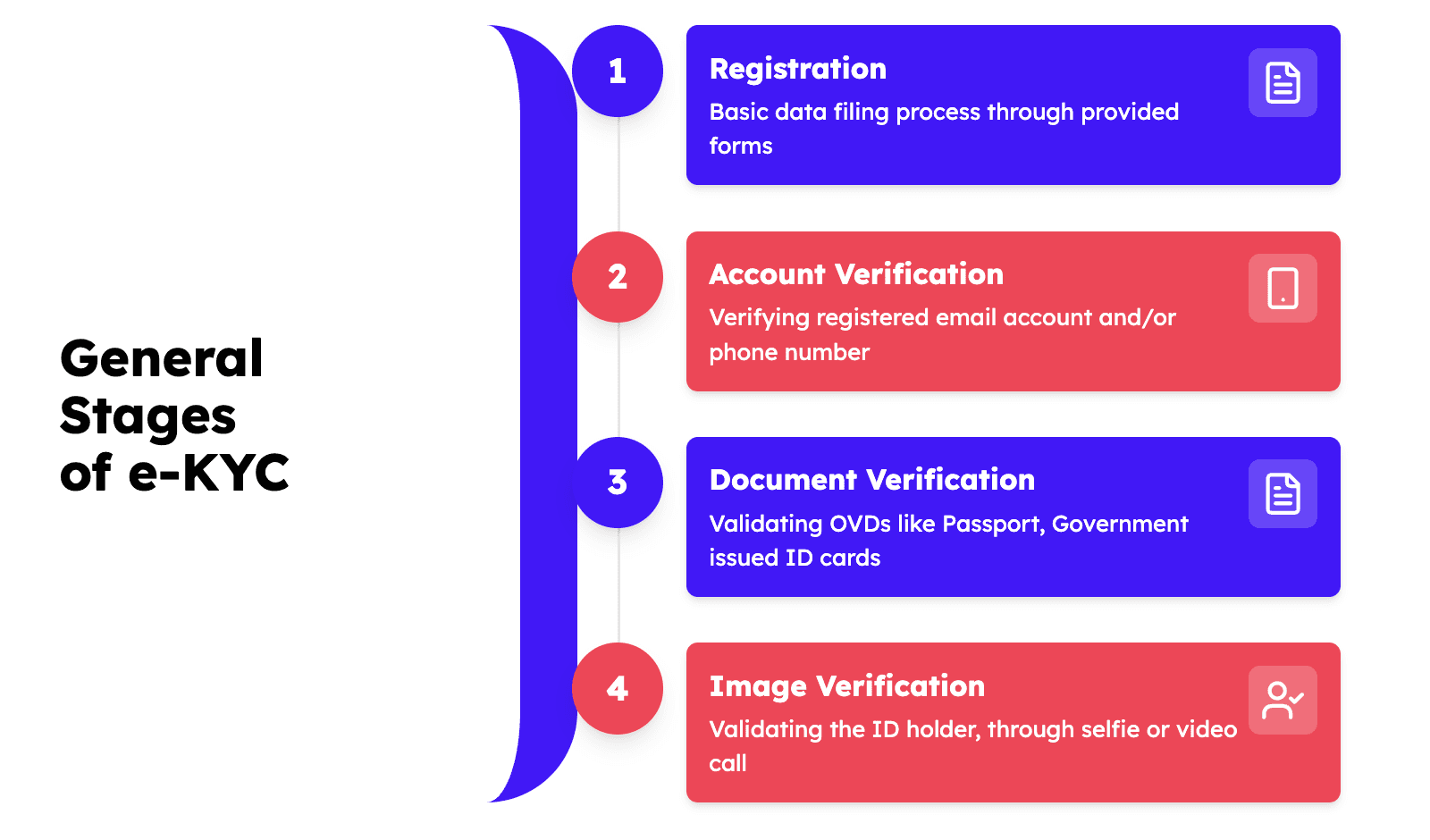

Know Your Customer, or KYC, is the process of verifying customer identities that enables digital businesses, especially financial institutions, to stop fraud and meet regulatory obligations. However, for businesses with cross-border operations, KYC may get tricky.

In this dynamic market landscape, where each geographical region has unique and evolving laws, tech landscapes, and fraud risks, it is essential that businesses understand region-specific KYC requirements or collaborate with partners like Bureau to navigate the complexities of regional KYC requirements with precision and ease.

?

Understanding regional KYC requirements

KYC is an important tool in fraud prevention, enabling businesses to block criminal activities, such as money laundering, and maintain a trustworthy digital platform for their users. The first step, therefore, is to understand jurisdiction-specific laws and KYC requirements, as explained below:

The USA

KYC in the United States is governed by the Bank Secrecy Act and the USA PATRIOT Act. These regulations apply to both domestic and foreign financial institutions that operate within the U.S. or maintain correspondent accounts with U.S. banks. To combat money laundering and terrorist financingm institutions are required to:

Verify Customer Identities,

Monitor Transactions,

Report Suspicious Activity

European Union

The EU’s KYC requirements are a combination of anti-money laundering directives and GDPR’s data privacy rules. Financial institutions in the member countries must follow the EU’s AML laws as well as country-specific rules when conducting identity checks. They must continuously monitor user interactions, and ensure compliance with the GDPR guidelines on the collection and usage of users’ personal data.

Australia

The Anti-Money Laundering and Counter-Terrorism Financing Act governs KYC in Australia. It requires financial institutions and fintechs verify identities, assess risks, and report oddities.

India

India’s central bank, the Reserve Bank of India prescribes verifying documents like Aadhaar or PAN (permanent account number) cards in addition to rigorous anti-money laundering steps, as part of KYC checks in India.

Middle East and North Africa (MENA)

The MENA region presents a diverse regulatory landscape concerning Know Your Customer (KYC) practices. While some countries have established robust frameworks, others are in the process of developing comprehensive regulations. Below is a country-specific breakdown:

Saudi Arabia

In Saudi Arabia, the KYC process is governed by the Saudi Central Bank (SAMA). Financial institutions are mandated to:

Customer Identification: Collect and verify personal details, including name, date of birth, nationality, and occupation.

Document Verification: Obtain official identification documents, such as a valid passport or national ID card, and verify their authenticity.

Address Verification: Confirm residential details through utility bills, bank statements, or other official documents.

Risk Assessment: Evaluate potential risks associated with the customer's financial activities, considering factors like source of income and political exposure.

Ongoing Monitoring: Continuously monitor customer transactions to detect and report suspicious activities.

Record Keeping: Maintain comprehensive records of customer information and KYC documentation for regulatory inspections and investigations.

Non-compliance with these regulations can result in severe penalties, including fines and imprisonment.

United Arab Emirates (UAE)

The UAE has implemented stringent KYC regulations overseen by the Central Bank of the UAE (CBUAE). Key requirements include:

Customer Due Diligence (CDD): Obligates financial institutions to identify and verify the identity of their customers.

Enhanced Due Diligence (EDD): Requires additional scrutiny for high-risk customers, including those involved in complex transactions or from high-risk countries.

Ongoing Monitoring: Mandates continuous monitoring of transactions to ensure they align with the customer's profile and to identify any unusual activity.

Record Keeping: Institutions must retain records of all transactions and customer information for a minimum of five years.

Failure to adhere to these regulations can lead to significant penalties, including fines and imprisonment.

Qatar

Qatar's financial institutions are regulated by the Qatar Central Bank (QCB), which enforces KYC requirements to prevent money laundering and terrorist financing. Institutions must conduct thorough customer identification and verification processes, monitor transactions, and report any suspicious activities to the Financial Information Unit (FIU).

Kuwait

In Kuwait, the Central Bank of Kuwait (CBK) mandates financial institutions to implement KYC procedures, including customer identification, risk assessment, and transaction monitoring. The regulations aim to align with international standards to combat financial crimes.

Bahrain

The Central Bank of Bahrain (CBB) oversees KYC regulations, requiring financial institutions to perform due diligence, maintain accurate records, and report suspicious transactions. The CBB's framework is designed to ensure transparency and integrity within the financial sector.

Oman

Oman's financial institutions are governed by the Central Bank of Oman (CBO), which enforces KYC regulations to identify and verify customers, assess risks, and monitor transactions. The CBO emphasizes the importance of compliance to safeguard the financial system against illicit activities.

Egypt

The Central Bank of Egypt (CBE) requires financial institutions to implement KYC procedures, including customer identification, verification, and ongoing monitoring. The regulations aim to enhance the stability and security of Egypt's financial sector.

This country-specific breakdown highlights the varying degrees of KYC regulation implementation across the MENA region. While some countries have established comprehensive frameworks, others continue to develop and refine their regulatory approaches to align with international standards.

Southeast Asia (SEA)

KYC regulations across Southeast Asia vary significantly. While countries like Singapore have established stringent frameworks, others are in the process of enhancing their regulatory measures. Below is a country-specific breakdown:

Malaysia

Malaysia's KYC framework is governed by the Anti-Money Laundering, Anti-Terrorism Financing and Proceeds of Unlawful Activities Act 2001 (AMLA), the Financial Services Act 2013 (FSA), and the Islamic Financial Services Act 2013 (IFSA). These laws impose AML/CFT requirements on financial institutions, including customer due diligence measures, record keeping, and reporting obligations.

Bank Negara Malaysia (BNM) has issued a revised policy document on electronic Know-Your-Customer (e-KYC) to facilitate digital onboarding. The policy outlines minimum requirements and standards for implementing e-KYC solutions, including document verification, biometric matching, and liveness detection. Financial institutions must obtain board approval for their e-KYC frameworks and ensure compliance with the policy's safeguards, especially for higher-risk financial products.

Singapore

Singapore's KYC regulations are overseen by the Monetary Authority of Singapore (MAS) under the Prevention of Money Laundering and Countering the Financing of Terrorism Act of 2007. Financial institutions are required to verify customer identities, monitor transactions, and report suspicious activities.

The Payment Services Act (PSA) of 2019 expanded the regulatory framework to include digital payment services, requiring entities to implement robust KYC measures. Singapore's National Digital Identity (NDI) program, featuring Singpass, facilitates secure digital identity verification for online services.

Non-compliance with KYC regulations can result in severe penalties, including fines, revocation of licenses, and criminal charges.

Thailand

Thailand's KYC regulations are enforced by the Anti-Money Laundering Office (AMLO) and the Bank of Thailand. Financial institutions must conduct customer due diligence, verify identification documents, and monitor transactions for suspicious activities.

Recent regulations mandate the use of electronic KYC (e-KYC) processes, including biometric verification and smart card readers, for digital onboarding. Financial institutions are required to implement effective risk management systems to ensure the accuracy and security of customer identification.

Indonesia

Indonesia's KYC framework is governed by the Financial Services Authority (OJK) and Bank Indonesia. Financial institutions are mandated to verify customer identities, assess risk profiles, and monitor transactions to prevent money laundering and terrorism financing.

The implementation of electronic KYC (e-KYC) processes has been emphasized to enhance efficiency and accuracy in customer verification. Financial institutions are required to adopt robust identity verification and customer due diligence measures, including the use of biometric data and digital identification systems.

Vietnam

Vietnam has strengthened its anti-money laundering (AML) framework with the introduction of the Anti-Money Laundering Law 2022 and the Law on Credit Institutions 2024. These laws enhance AML monitoring processes and aim to improve banking operations and transparency.

Financial institutions are required to implement customer due diligence measures, including identity verification and transaction monitoring. Recent regulations mandate biometric verification for digital transactions exceeding certain thresholds to enhance security and prevent illicit activities.

Philippines

The Bangko Sentral ng Pilipinas (BSP) oversees KYC regulations in the Philippines. Financial institutions are required to establish and record the true identity of their clients based on official documents. The BSP has issued guidelines to strengthen the financial system's defenses against money laundering and terrorist financing.

Recent amendments to the Manual of Regulations for Banks (MORB) and Non-Bank Financial Institutions (MORNBFI) include guidelines on electronic KYC (e-KYC) using digital identity systems, such as the Philippines' national ID, PhilSys. These updates aim to facilitate secure and efficient customer onboarding processes.

?

This country-specific breakdown highlights the varying degrees of KYC regulation implementation across Southeast Asia. While some countries have established comprehensive frameworks, others continue to develop and refine their regulatory approaches to align with international standards.

?

Challenges in meeting regional KYC requirements

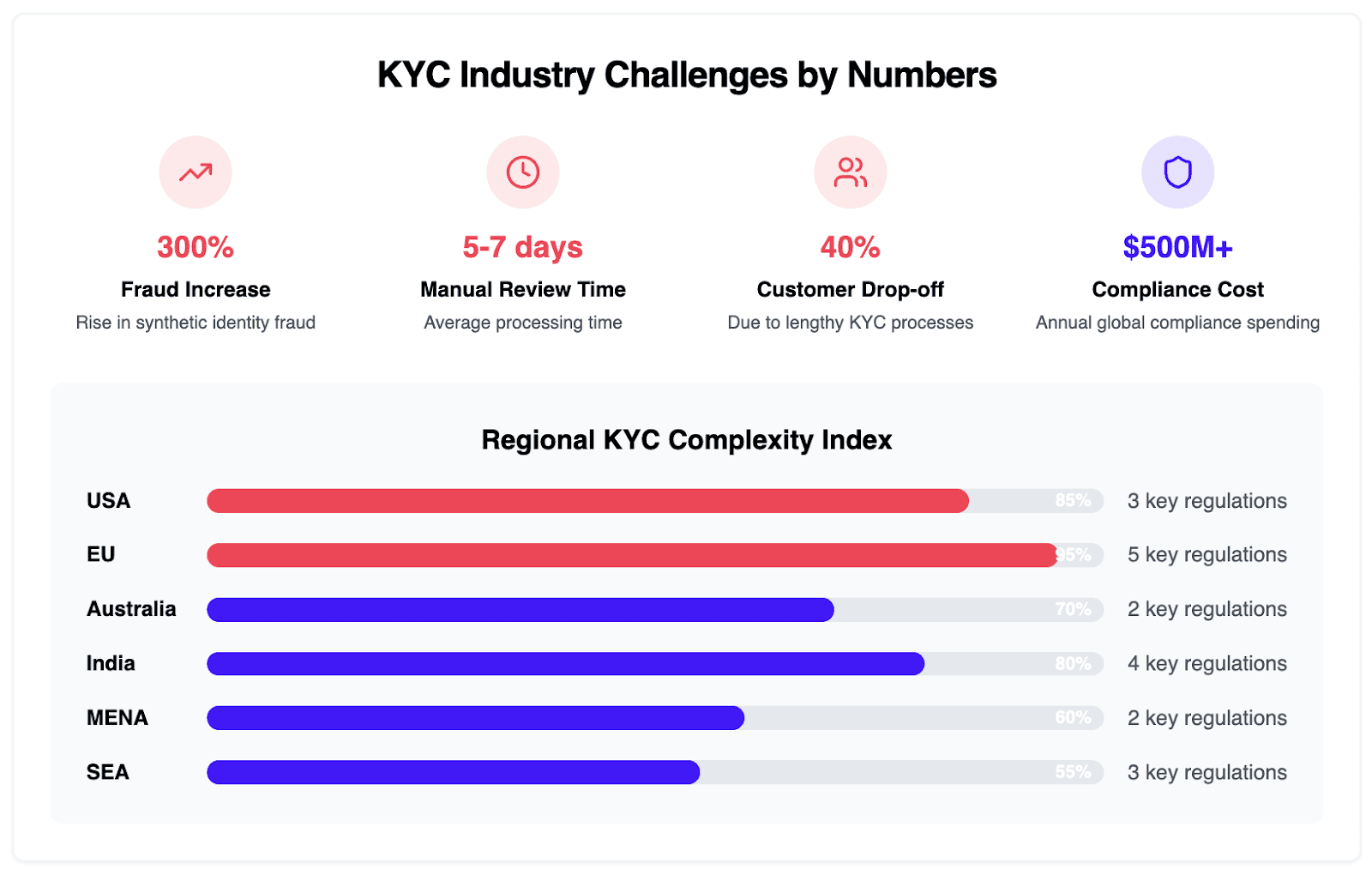

Digital fraud continues to evolve, while the defenses are mostly static and fail to keep pace with the modern attack techniques such as synthetic identities and AI-generated deepfakes. Many businesses worldwide still rely on manual reviews that delay onboarding, are labor-intensive, costly, and often result in customer discontent. Moreover, they allow fraudsters to exploit the loopholes and blend with genuine users to pass through undetected.

Businesses must also seek customer consent, such as in the EU, before being able to process user data. This not only degrades user experience due to the time drag but may also result in customer churn.

Inconsistent regulations, such as in the EU, MENA and SEA regions, make KYC checks market- or country-driven, opening up lacunae for bad actors to take advantage of. Similarly in India and Australia, with large rural populations that lack digital infrastructure or digital know-how, KYC checks can prove onerous.

Fraud thrives in chaos. And the complexity created by disparate laws and jurisdiction-specific regulations make it harder for businesses to balance fraud prevention with compliance. Therefore, there is an urgent need for compliance-ready solutions that streamline the KYC processes and allow businesses to focus on expansion.

?

Stay compliant with Bureau’s KYC stack

With a KYC stack that spans over 190+ countries, Bureau’s unified risk decisioning platform caters to the diverse KYC requirements across geographical regions. It leverages AI to aggregate relevant regional data and combines the threat intelligence from Bureau’s global network to keep businesses compliant with their regulatory obligations.

Bureau’s expertise in meeting regional KYC requirements stems from its support for over 2,000 document types across 190+ countries and access to reliable private, public, and government databases. This allows businesses to stay compliant and reduce fraud across global markets, whether operating under the US Patriot Act, Europe’s GDPR, India’s RBI guidelines, or local rules in MENA and Southeast Asia.

Key advantages:

Broad document coverage

Covers more than 2,000 identity document types, including passports, national IDs, and licenses, tailored to local standards in over 190 countries.Trusted data verification

Uses verified sources from government, private, and public databases to authenticate identities and reduce false positives.Compliance across regions

Meets strict regulatory requirements in the US, Europe, and India, and adapts to country-specific mandates in markets across MENA and SEA.Region-aware verification

Adjusts risk thresholds and verification methods based on the reliability of local documents and fraud trends.One platform for global KYC

Allows businesses to manage KYC across multiple markets through a single, integrated solution that scales with growth.

?

By streamlining the KYC process and customizing workflows, Bureau allows businesses to improve catch rates, reduce manual burden and associated costs, and maintain a seamless user experience, no matter the region.

For faster, user-centric, and compliant KYC checks, Contact Bureau Now.

?

With a KYC stack that supports 2,000+ document types in 190+ countries, Bureau’s unified risk decisioning platform helps businesses maintain compliance with local, regional, and global KYC requirements

Know Your Customer, or KYC, is the process of verifying customer identities that enables digital businesses, especially financial institutions, to stop fraud and meet regulatory obligations. However, for businesses with cross-border operations, KYC may get tricky.

In this dynamic market landscape, where each geographical region has unique and evolving laws, tech landscapes, and fraud risks, it is essential that businesses understand region-specific KYC requirements or collaborate with partners like Bureau to navigate the complexities of regional KYC requirements with precision and ease.

?

Understanding regional KYC requirements

KYC is an important tool in fraud prevention, enabling businesses to block criminal activities, such as money laundering, and maintain a trustworthy digital platform for their users. The first step, therefore, is to understand jurisdiction-specific laws and KYC requirements, as explained below:

The USA

KYC in the United States is governed by the Bank Secrecy Act and the USA PATRIOT Act. These regulations apply to both domestic and foreign financial institutions that operate within the U.S. or maintain correspondent accounts with U.S. banks. To combat money laundering and terrorist financingm institutions are required to:

Verify Customer Identities,

Monitor Transactions,

Report Suspicious Activity

European Union

The EU’s KYC requirements are a combination of anti-money laundering directives and GDPR’s data privacy rules. Financial institutions in the member countries must follow the EU’s AML laws as well as country-specific rules when conducting identity checks. They must continuously monitor user interactions, and ensure compliance with the GDPR guidelines on the collection and usage of users’ personal data.

Australia

The Anti-Money Laundering and Counter-Terrorism Financing Act governs KYC in Australia. It requires financial institutions and fintechs verify identities, assess risks, and report oddities.

India

India’s central bank, the Reserve Bank of India prescribes verifying documents like Aadhaar or PAN (permanent account number) cards in addition to rigorous anti-money laundering steps, as part of KYC checks in India.

Middle East and North Africa (MENA)

The MENA region presents a diverse regulatory landscape concerning Know Your Customer (KYC) practices. While some countries have established robust frameworks, others are in the process of developing comprehensive regulations. Below is a country-specific breakdown:

Saudi Arabia

In Saudi Arabia, the KYC process is governed by the Saudi Central Bank (SAMA). Financial institutions are mandated to:

Customer Identification: Collect and verify personal details, including name, date of birth, nationality, and occupation.

Document Verification: Obtain official identification documents, such as a valid passport or national ID card, and verify their authenticity.

Address Verification: Confirm residential details through utility bills, bank statements, or other official documents.

Risk Assessment: Evaluate potential risks associated with the customer's financial activities, considering factors like source of income and political exposure.

Ongoing Monitoring: Continuously monitor customer transactions to detect and report suspicious activities.

Record Keeping: Maintain comprehensive records of customer information and KYC documentation for regulatory inspections and investigations.

Non-compliance with these regulations can result in severe penalties, including fines and imprisonment.

United Arab Emirates (UAE)

The UAE has implemented stringent KYC regulations overseen by the Central Bank of the UAE (CBUAE). Key requirements include:

Customer Due Diligence (CDD): Obligates financial institutions to identify and verify the identity of their customers.

Enhanced Due Diligence (EDD): Requires additional scrutiny for high-risk customers, including those involved in complex transactions or from high-risk countries.

Ongoing Monitoring: Mandates continuous monitoring of transactions to ensure they align with the customer's profile and to identify any unusual activity.

Record Keeping: Institutions must retain records of all transactions and customer information for a minimum of five years.

Failure to adhere to these regulations can lead to significant penalties, including fines and imprisonment.

Qatar

Qatar's financial institutions are regulated by the Qatar Central Bank (QCB), which enforces KYC requirements to prevent money laundering and terrorist financing. Institutions must conduct thorough customer identification and verification processes, monitor transactions, and report any suspicious activities to the Financial Information Unit (FIU).

Kuwait

In Kuwait, the Central Bank of Kuwait (CBK) mandates financial institutions to implement KYC procedures, including customer identification, risk assessment, and transaction monitoring. The regulations aim to align with international standards to combat financial crimes.

Bahrain

The Central Bank of Bahrain (CBB) oversees KYC regulations, requiring financial institutions to perform due diligence, maintain accurate records, and report suspicious transactions. The CBB's framework is designed to ensure transparency and integrity within the financial sector.

Oman

Oman's financial institutions are governed by the Central Bank of Oman (CBO), which enforces KYC regulations to identify and verify customers, assess risks, and monitor transactions. The CBO emphasizes the importance of compliance to safeguard the financial system against illicit activities.

Egypt

The Central Bank of Egypt (CBE) requires financial institutions to implement KYC procedures, including customer identification, verification, and ongoing monitoring. The regulations aim to enhance the stability and security of Egypt's financial sector.

This country-specific breakdown highlights the varying degrees of KYC regulation implementation across the MENA region. While some countries have established comprehensive frameworks, others continue to develop and refine their regulatory approaches to align with international standards.

Southeast Asia (SEA)

KYC regulations across Southeast Asia vary significantly. While countries like Singapore have established stringent frameworks, others are in the process of enhancing their regulatory measures. Below is a country-specific breakdown:

Malaysia

Malaysia's KYC framework is governed by the Anti-Money Laundering, Anti-Terrorism Financing and Proceeds of Unlawful Activities Act 2001 (AMLA), the Financial Services Act 2013 (FSA), and the Islamic Financial Services Act 2013 (IFSA). These laws impose AML/CFT requirements on financial institutions, including customer due diligence measures, record keeping, and reporting obligations.

Bank Negara Malaysia (BNM) has issued a revised policy document on electronic Know-Your-Customer (e-KYC) to facilitate digital onboarding. The policy outlines minimum requirements and standards for implementing e-KYC solutions, including document verification, biometric matching, and liveness detection. Financial institutions must obtain board approval for their e-KYC frameworks and ensure compliance with the policy's safeguards, especially for higher-risk financial products.

Singapore

Singapore's KYC regulations are overseen by the Monetary Authority of Singapore (MAS) under the Prevention of Money Laundering and Countering the Financing of Terrorism Act of 2007. Financial institutions are required to verify customer identities, monitor transactions, and report suspicious activities.

The Payment Services Act (PSA) of 2019 expanded the regulatory framework to include digital payment services, requiring entities to implement robust KYC measures. Singapore's National Digital Identity (NDI) program, featuring Singpass, facilitates secure digital identity verification for online services.

Non-compliance with KYC regulations can result in severe penalties, including fines, revocation of licenses, and criminal charges.

Thailand

Thailand's KYC regulations are enforced by the Anti-Money Laundering Office (AMLO) and the Bank of Thailand. Financial institutions must conduct customer due diligence, verify identification documents, and monitor transactions for suspicious activities.

Recent regulations mandate the use of electronic KYC (e-KYC) processes, including biometric verification and smart card readers, for digital onboarding. Financial institutions are required to implement effective risk management systems to ensure the accuracy and security of customer identification.

Indonesia

Indonesia's KYC framework is governed by the Financial Services Authority (OJK) and Bank Indonesia. Financial institutions are mandated to verify customer identities, assess risk profiles, and monitor transactions to prevent money laundering and terrorism financing.

The implementation of electronic KYC (e-KYC) processes has been emphasized to enhance efficiency and accuracy in customer verification. Financial institutions are required to adopt robust identity verification and customer due diligence measures, including the use of biometric data and digital identification systems.

Vietnam

Vietnam has strengthened its anti-money laundering (AML) framework with the introduction of the Anti-Money Laundering Law 2022 and the Law on Credit Institutions 2024. These laws enhance AML monitoring processes and aim to improve banking operations and transparency.

Financial institutions are required to implement customer due diligence measures, including identity verification and transaction monitoring. Recent regulations mandate biometric verification for digital transactions exceeding certain thresholds to enhance security and prevent illicit activities.

Philippines

The Bangko Sentral ng Pilipinas (BSP) oversees KYC regulations in the Philippines. Financial institutions are required to establish and record the true identity of their clients based on official documents. The BSP has issued guidelines to strengthen the financial system's defenses against money laundering and terrorist financing.

Recent amendments to the Manual of Regulations for Banks (MORB) and Non-Bank Financial Institutions (MORNBFI) include guidelines on electronic KYC (e-KYC) using digital identity systems, such as the Philippines' national ID, PhilSys. These updates aim to facilitate secure and efficient customer onboarding processes.

?

This country-specific breakdown highlights the varying degrees of KYC regulation implementation across Southeast Asia. While some countries have established comprehensive frameworks, others continue to develop and refine their regulatory approaches to align with international standards.

?

Challenges in meeting regional KYC requirements

Digital fraud continues to evolve, while the defenses are mostly static and fail to keep pace with the modern attack techniques such as synthetic identities and AI-generated deepfakes. Many businesses worldwide still rely on manual reviews that delay onboarding, are labor-intensive, costly, and often result in customer discontent. Moreover, they allow fraudsters to exploit the loopholes and blend with genuine users to pass through undetected.

Businesses must also seek customer consent, such as in the EU, before being able to process user data. This not only degrades user experience due to the time drag but may also result in customer churn.

Inconsistent regulations, such as in the EU, MENA and SEA regions, make KYC checks market- or country-driven, opening up lacunae for bad actors to take advantage of. Similarly in India and Australia, with large rural populations that lack digital infrastructure or digital know-how, KYC checks can prove onerous.

Fraud thrives in chaos. And the complexity created by disparate laws and jurisdiction-specific regulations make it harder for businesses to balance fraud prevention with compliance. Therefore, there is an urgent need for compliance-ready solutions that streamline the KYC processes and allow businesses to focus on expansion.

?

Stay compliant with Bureau’s KYC stack

With a KYC stack that spans over 190+ countries, Bureau’s unified risk decisioning platform caters to the diverse KYC requirements across geographical regions. It leverages AI to aggregate relevant regional data and combines the threat intelligence from Bureau’s global network to keep businesses compliant with their regulatory obligations.

Bureau’s expertise in meeting regional KYC requirements stems from its support for over 2,000 document types across 190+ countries and access to reliable private, public, and government databases. This allows businesses to stay compliant and reduce fraud across global markets, whether operating under the US Patriot Act, Europe’s GDPR, India’s RBI guidelines, or local rules in MENA and Southeast Asia.

Key advantages:

Broad document coverage

Covers more than 2,000 identity document types, including passports, national IDs, and licenses, tailored to local standards in over 190 countries.Trusted data verification

Uses verified sources from government, private, and public databases to authenticate identities and reduce false positives.Compliance across regions

Meets strict regulatory requirements in the US, Europe, and India, and adapts to country-specific mandates in markets across MENA and SEA.Region-aware verification

Adjusts risk thresholds and verification methods based on the reliability of local documents and fraud trends.One platform for global KYC

Allows businesses to manage KYC across multiple markets through a single, integrated solution that scales with growth.

?

By streamlining the KYC process and customizing workflows, Bureau allows businesses to improve catch rates, reduce manual burden and associated costs, and maintain a seamless user experience, no matter the region.

For faster, user-centric, and compliant KYC checks, Contact Bureau Now.

?

TABLE OF CONTENTS

See More

Recommended Blogs

Landing Page.

Simple, bold.

Sign Up

Download

Products

Solutions

Resources

© 2026 Bureau . All rights reserved.

Solutions

Industries

Resources

Company

Solutions

Industries

Resources

Company

© 2026 Bureau . All rights reserved.

Follow Us

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

© 2026 Bureau . All rights reserved.