Enhanced Due Diligence Explained: A KYC Compliance Guide for 2024

Enhanced Due Diligence Explained: A KYC Compliance Guide for 2024

Enhanced Due Diligence Explained: A KYC Compliance Guide for 2024

When basic identity checks fall short, businesses must go the extra mile with enhanced due diligence to assess customer risk effectively.

Author

Rahi Bhattacharjee

See how Bureau has helped industry leaders defend against networked Industrial-scale frauds →

Schedule a Demo

TABLE OF CONTENTS

See Less

A most basic part of the Know-Your-Customer (KYC) process is the Customer Due Diligence (CDD) where a customer is asked for their full name, contact details, place and date of birth, nationality, and marital status and this is verified against a government database. When these checks fall short, businesses must go the extra mile to secure their interests by conducting a more thorough assessment of the customer. This extension of KYC is known as Enhanced Due Diligence (EDD).

Why is it necessary, you ask? Billions of dollars are moved through the global financial ecosystem using illegal methods. Despite the comprehensive measures taken by regulators and law enforcement, it falls short in the face of sophisticated fraudulent methods. Each financial institution has their own KYC and Anti Money Laundering (AML) process and guidelines in place that they follow. These guidelines help victims from falling prey to financial fraud because the basic KYC and CDD were not enough. Identities can be stolen and data can be faked. This is were EDD comes in.

Here’s a detailed breakdown of what is EDD and why is it important.

What is Enhanced Due Diligence (EDD)?

Enhanced Due diligence (EDD) is a KYC process that takes a risk-based approach to gather and analyze information about potential clients. During EDD, the company asks for more information than usual to mitigate and prevent financial crime. EDD goes beyond traditional identity verification and goes deeper into the potential client’s background to prevent them from engaging in financial crimes like money laundering, payment fraud, account takeovers, money mule activity, and more.

A simple example of why EDD might be more relevant than CDD would be in the case of New to credit/ New to finance individuals. Since they don't have existing bank accounts or financial activity, they cannot be evaluated based on usual factors like credit score, bank activity, loan repayment history etc.

For these customers, businesses need to gather additional information based on their mobile devices, sim card, occupation proof etc.

What is the purpose of Enhanced Due Diligence (EDD)?

The desired result of the EDD process is to provide a 360° overview of the customer’s source of wealth, funds, the nature of their business, their financial activity, connections to relevant high-profile individuals, and more.

The extensive intelligence provided by EDD helps reduce the vulnerabilities of financial institutions by identifying suspicious activities and stopping the crime before it can cause irreparable damage. This process of enhanced verification is especially performed for high-risk customers.

Also read: Safeguarding Your Fintech World: Tackling Identity Theft Head-On!

Who are high-risk customers? (And examples)

High-risk customers have a higher potential of committing financial crimes. There are certain attributes about an individual that are taken into account when categorizing them as high-risk customers.

Here are some examples of high-risk customers:

1. Politically Exposed Persons (PEPs)

The Reserve Bank of India recently clarified what ‘Politically Exposed Persons’ means to meet the Financial Action Task Force (FATF) norms. Political Exposed People have a prominent position in public life including heads of states/governments, senior politicians, senior governments, judicial or military officers, senior executives of state-owned corporations, and high-profile political party officials.

These customers can potentially abuse their positions by becoming fronts of money laundering and committing related crimes like bribery and corruption.

2. Customers linked to high-risk countries

Individuals who are linked to countries that have a history of fraudulent activity or are hubs of terrorism are at higher risk of becoming agents of financial terrorism. The FATF has two lists of countries that they classify as “high risk”. The governments of these countries are encouraged to actively work with the FATF to address the deficiencies in their regimes to counter money laundering, terrorist financing, and proliferation financing.

The ‘black list’ has 3 countries in 2024: Iran, Myanmar, and the Democratic People’s Republic of Korea.

The ‘grey list’ has 21 countries. Find the list of countries here.

3. Customers linked to high-risk business sectors

Some business sectors show higher money laundering activity than others. These sectors usually have a high rate of unregistered businesses, and informal business activities and are cash-intensive. Customers linked to these sectors are considered high-risk.

4. Customers linked to businesses with complex ownership structures

Complex business structures are an excellent way to mask money laundering trails. Customers linked to such organizations can become mules in money laundering activity.

In India, the central financial authority - the Reserve Bank of India, regularly updates its KYC guidelines to stay vigilant. In a recent update, the RBI mandated that all Reporting Entities and concerned authorities would have to take reasonable steps to determine whether a customer is acting on behalf of a beneficial owner and would also take all steps to verify the identity of the beneficial owner, using reliable and independent sources.

5. Customers with unusual bank activity

These customers usually show bank accounts that show anomalies in their financial transactions. For example, if a dormant account suddenly receives a large volume of transactions. Or if their bank accounts abruptly show signs of transactions to other countries, or other high-risk individuals.

According to AML guidelines by global organizations, individuals with the above characteristics must undergo more thorough identity verification to ensure they don't engage in fraudulent activities instead of a usual Customer Due Diligence as part of the KYC process.

?

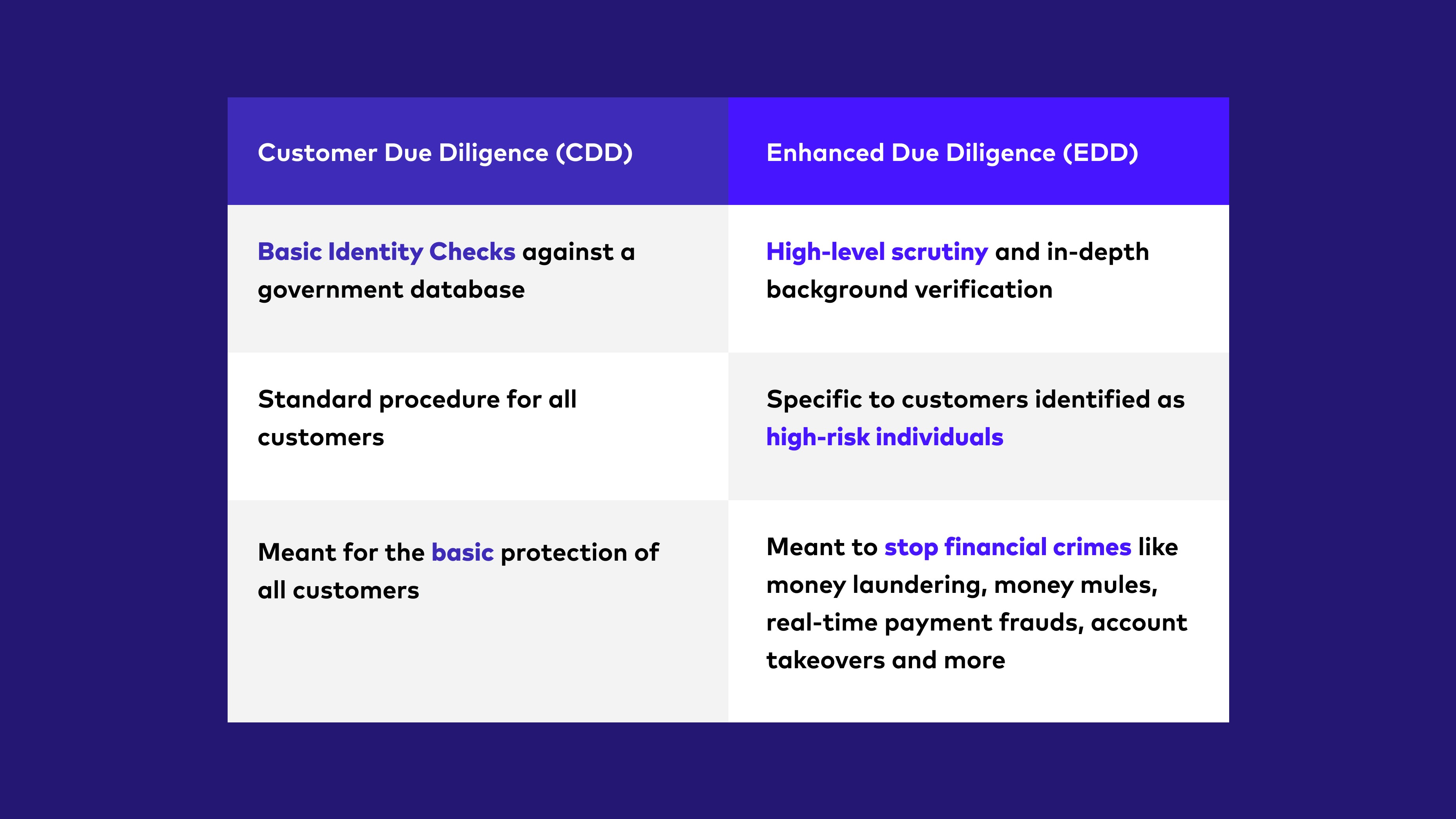

What is the difference between CDD and EDD?

The fundamental difference between Customer Due Diligence (CDD) and Enhanced Due Diligence (EDD) lies in the level of scrutiny that a customer has to go through for background verification at the time of onboarding.

Customer Due Diligence is the fundamental identity verification process that any customer who will conduct any kind of financial transaction will have to undergo. It is a part of the Know Your Customer process where the customer’s identity is verified against government-verified data.

On the other hand, Enhanced Due Diligence is additional scrutiny that customers who are considered “high-risk individuals” have to undergo.

?

Difference between Customer Due diligence and Enhanced Due diligence

?

?

Bureau: A Regtech Solution For Enhanced Due Diligence

Compliance and fraud prevention go hand-in-hand. Bureau’s comprehensive solutions form an additional layer of defence over existing AML and KYC checks to ensure fraudsters do not slip through the crack when dealing with a massive magnitude of data.

Bureau analyses 200+ risk signals pertaining to a user’s email, phone number, identity documents, along with peripheral signals such as device integrity and behaviour patterns to provide a cumulative risk score that helps banks and FIs verify the legitimacy of a customer.

Our latest solution Money Mule Score has been a revolutionary asset in helping stop financial crime like money laundering activity in its tracks.

?

See how Bureau is fighting fraud!

?

A most basic part of the Know-Your-Customer (KYC) process is the Customer Due Diligence (CDD) where a customer is asked for their full name, contact details, place and date of birth, nationality, and marital status and this is verified against a government database. When these checks fall short, businesses must go the extra mile to secure their interests by conducting a more thorough assessment of the customer. This extension of KYC is known as Enhanced Due Diligence (EDD).

Why is it necessary, you ask? Billions of dollars are moved through the global financial ecosystem using illegal methods. Despite the comprehensive measures taken by regulators and law enforcement, it falls short in the face of sophisticated fraudulent methods. Each financial institution has their own KYC and Anti Money Laundering (AML) process and guidelines in place that they follow. These guidelines help victims from falling prey to financial fraud because the basic KYC and CDD were not enough. Identities can be stolen and data can be faked. This is were EDD comes in.

Here’s a detailed breakdown of what is EDD and why is it important.

What is Enhanced Due Diligence (EDD)?

Enhanced Due diligence (EDD) is a KYC process that takes a risk-based approach to gather and analyze information about potential clients. During EDD, the company asks for more information than usual to mitigate and prevent financial crime. EDD goes beyond traditional identity verification and goes deeper into the potential client’s background to prevent them from engaging in financial crimes like money laundering, payment fraud, account takeovers, money mule activity, and more.

A simple example of why EDD might be more relevant than CDD would be in the case of New to credit/ New to finance individuals. Since they don't have existing bank accounts or financial activity, they cannot be evaluated based on usual factors like credit score, bank activity, loan repayment history etc.

For these customers, businesses need to gather additional information based on their mobile devices, sim card, occupation proof etc.

What is the purpose of Enhanced Due Diligence (EDD)?

The desired result of the EDD process is to provide a 360° overview of the customer’s source of wealth, funds, the nature of their business, their financial activity, connections to relevant high-profile individuals, and more.

The extensive intelligence provided by EDD helps reduce the vulnerabilities of financial institutions by identifying suspicious activities and stopping the crime before it can cause irreparable damage. This process of enhanced verification is especially performed for high-risk customers.

Also read: Safeguarding Your Fintech World: Tackling Identity Theft Head-On!

Who are high-risk customers? (And examples)

High-risk customers have a higher potential of committing financial crimes. There are certain attributes about an individual that are taken into account when categorizing them as high-risk customers.

Here are some examples of high-risk customers:

1. Politically Exposed Persons (PEPs)

The Reserve Bank of India recently clarified what ‘Politically Exposed Persons’ means to meet the Financial Action Task Force (FATF) norms. Political Exposed People have a prominent position in public life including heads of states/governments, senior politicians, senior governments, judicial or military officers, senior executives of state-owned corporations, and high-profile political party officials.

These customers can potentially abuse their positions by becoming fronts of money laundering and committing related crimes like bribery and corruption.

2. Customers linked to high-risk countries

Individuals who are linked to countries that have a history of fraudulent activity or are hubs of terrorism are at higher risk of becoming agents of financial terrorism. The FATF has two lists of countries that they classify as “high risk”. The governments of these countries are encouraged to actively work with the FATF to address the deficiencies in their regimes to counter money laundering, terrorist financing, and proliferation financing.

The ‘black list’ has 3 countries in 2024: Iran, Myanmar, and the Democratic People’s Republic of Korea.

The ‘grey list’ has 21 countries. Find the list of countries here.

3. Customers linked to high-risk business sectors

Some business sectors show higher money laundering activity than others. These sectors usually have a high rate of unregistered businesses, and informal business activities and are cash-intensive. Customers linked to these sectors are considered high-risk.

4. Customers linked to businesses with complex ownership structures

Complex business structures are an excellent way to mask money laundering trails. Customers linked to such organizations can become mules in money laundering activity.

In India, the central financial authority - the Reserve Bank of India, regularly updates its KYC guidelines to stay vigilant. In a recent update, the RBI mandated that all Reporting Entities and concerned authorities would have to take reasonable steps to determine whether a customer is acting on behalf of a beneficial owner and would also take all steps to verify the identity of the beneficial owner, using reliable and independent sources.

5. Customers with unusual bank activity

These customers usually show bank accounts that show anomalies in their financial transactions. For example, if a dormant account suddenly receives a large volume of transactions. Or if their bank accounts abruptly show signs of transactions to other countries, or other high-risk individuals.

According to AML guidelines by global organizations, individuals with the above characteristics must undergo more thorough identity verification to ensure they don't engage in fraudulent activities instead of a usual Customer Due Diligence as part of the KYC process.

?

What is the difference between CDD and EDD?

The fundamental difference between Customer Due Diligence (CDD) and Enhanced Due Diligence (EDD) lies in the level of scrutiny that a customer has to go through for background verification at the time of onboarding.

Customer Due Diligence is the fundamental identity verification process that any customer who will conduct any kind of financial transaction will have to undergo. It is a part of the Know Your Customer process where the customer’s identity is verified against government-verified data.

On the other hand, Enhanced Due Diligence is additional scrutiny that customers who are considered “high-risk individuals” have to undergo.

?

Difference between Customer Due diligence and Enhanced Due diligence

?

?

Bureau: A Regtech Solution For Enhanced Due Diligence

Compliance and fraud prevention go hand-in-hand. Bureau’s comprehensive solutions form an additional layer of defence over existing AML and KYC checks to ensure fraudsters do not slip through the crack when dealing with a massive magnitude of data.

Bureau analyses 200+ risk signals pertaining to a user’s email, phone number, identity documents, along with peripheral signals such as device integrity and behaviour patterns to provide a cumulative risk score that helps banks and FIs verify the legitimacy of a customer.

Our latest solution Money Mule Score has been a revolutionary asset in helping stop financial crime like money laundering activity in its tracks.

?

See how Bureau is fighting fraud!

?

TABLE OF CONTENTS

See More

Recommended Blogs

Landing Page.

Simple, bold.

Sign Up

Download

Products

Solutions

Resources

© 2026 Bureau . All rights reserved.

Solutions

Industries

Resources

Company

Solutions

Industries

Resources

Company

© 2026 Bureau . All rights reserved.

Follow Us

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

© 2026 Bureau . All rights reserved.