What RBI's Payment Vision 2025 Means for India's Digital Future

What RBI's Payment Vision 2025 Means for India's Digital Future

What RBI's Payment Vision 2025 Means for India's Digital Future

The core theme of the 'Payment Vision 2025' document is 'E-Payments for Everyone, Everywhere, Every time'. At Bureau, we are working towards ushering in a new.

Author

Team Bureau

TABLE OF CONTENTS

See Less

A well-functioning payment system can aid in economic growth and promote financial inclusion. The need for such a system is accentuated in a developing country like India, where the JAM (Jan Dhan, Aadhaar and Mobile) trinity and low-cost mobile and data penetration have played a critical role in boosting the adoption of digital payments in the country. The UPI-enabled transactions in June 2022 were 5.86 billion in number and the transaction value exceeded Rs 10 lakh crores, registering an year-on-year growth of 108% and 85% respectively.

?

What is outlined in the Payments Vision 2025' document?

In its 'Payments Vision 2025' document, the Reserve Bank envisions a three-fold jump in digital payments and aims to establish India as a powerhouse of payments globally. The apex bank wants to make this rise in digital banking an irreversible shift without compromising the integrity of payment systems. It aims to improve the payment systems' reach, security, customer confidence and convenience.

?

As noted in the Vision document, India has one of the most modern payment systems in the world. The recent Phonepe-BCG report on digital payments expects the size to triple from US$3 trillion today to US$10 trillion by 2026.

?

With an enabling regulatory infrastructure and more significant usage of smartphones and mobile data, India witnessed an increase in the adoption of digital payments. And the Covid19 pandemic further accelerated the shift toward digital payments.

?

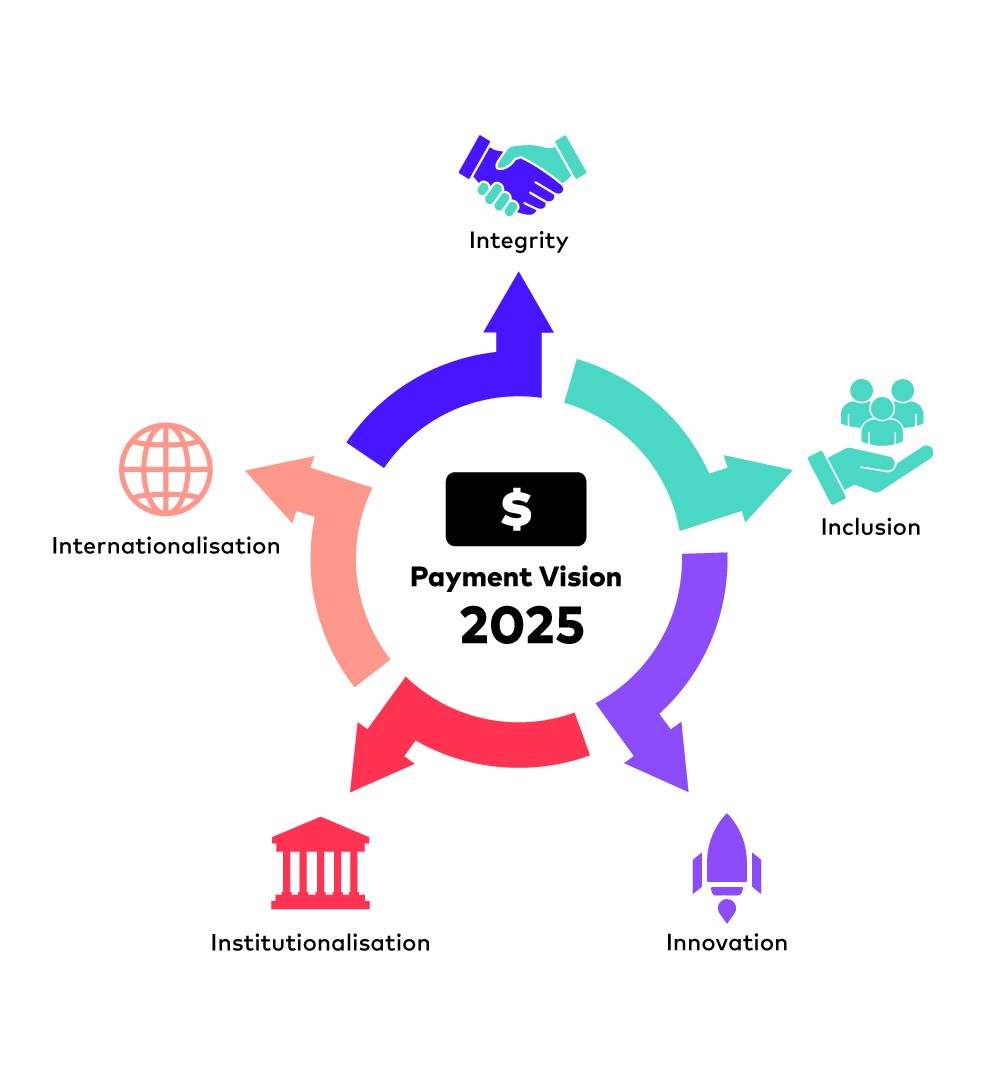

The 'Vision 2025' document is anchored on the five pillars – Integrity, Inclusion, Innovation, Institutionalisation and Internationalisation. Through these, the RBI intends to achieve ten outcomes, including growth of UPI at more than 50%, increase in PPI transactions by 150%, and the growth of registered customer base for mobile-based transactions by more than 50% per annum, among others.

Five pillars of Payment Vision 2025

Integrity

The integrity of payment systems is critical in strengthening customer confidence. To enhance the integrity of the payment systems, specific initiatives like the exploration of alternate risk-based authentication mechanisms, an 'Online Dispute Resolution' system for fraud monitoring and reporting and ring-fencing of domestic payment systems like the need to mandate domestic processing of payment transactions are envisaged.

?

Inclusion

The digital payment penetration in India exhibits a skewed pattern, with Tier III-VI cities having a lower penetration due to a lack of tech-savviness and an insufficient number of touchpoints. Recent initiatives like UPI123PAY (UPI payments for feature phone users) are expected to provide a fillip to the inclusion efforts. In addition, initiatives like a framework for geo-tagging of payment system touchpoints, review of guidelines on Prepaid Instruments (PPIs), and customer awareness activities are envisaged to deepen the access and usage of payment systems.

?

Innovation

Innovation in payment systems is needed to make payments more convenient and safe. The recent initiatives by RBI like opening up UPI for credit cards and organising hackathons like 'HARBINGER 2021 – Innovation for Transformation', aim to encourage innovation in the digital payment space. On the anvil are initiatives like reviewing the need for multiple payment identifiers (doing away with Indian Financial System Code (ISFC)) for fund transfers and IoT-based payments. The RBI is also expected to issue guidelines on payments involving BNPL soon.

?

Institutionalisation

The Payment and Settlements Act 2007, which governs the payment systems, would be reviewed according to the fast-changing payments landscape.

?

Internationalisation

RBI would support the expansion of UPI to countries across the world. Further, the widely anticipated launch of the Central Bank Digital Currency (CBDC) is expected to usher in greater efficiencies in domestic and cross-border payments and settlements.

To know more about CBDC, read Artificial Intelligence in CBDC.

?

How Bureau shares the vision

With the significant rise in digital payments in the last few years, the threat and fraud landscape has grown by leaps and bounds.

?

Every month, frauds worth more than Rs 200 crore are committed through UPI alone. Rising frauds, a lack of robust infrastructure to detect or prevent such instances, and the absence of a redressal mechanism are some of the concerns plaguing online digital payments. Moreover, fraudsters are becoming more sophisticated daily, using methods such as vishing, SIM cloning/swapping, malicious QR codes and apps, and more. Ironically, bad actors leverage the same technologies developed to build better consumer solutions.

?

Fortunately, there is also good news. New technologies are constantly emerging to keep us ahead of fraudsters. Bureau as an identity orchestration platform has been powering businesses to authenticate users and prevent fraud without adding friction to the customer's journey. Thus, Bureau's vision perfectly resonates with that of the RBI.

?

At Bureau, we believe fraud can be fought without increasing friction and sacrificing customer experience on the altar of risk.

?

Bureau is particularly seized by the problem of integrity in the digital world and the inadequacy of the current systems like SMS OTP. Bureau's One Tap Login (OTL) enables frictionless login that securely verifies mobile numbers leading to a sleek customer experience.

?

Bureau's onboarding platform works seamlessly and efficiently to verify KYC and comply with regulatory guidelines, including AML.

RBI’s vision of exploring alternate risk-based mechanisms like behavioural biometrics and location of the user for authentication is in sync with Bureau’s solution to reduce fraud. Bureau’s risk-based authentication uses risk scores based on rules that analyse various factors such as device, IP, phone number, and email id to determine if a user is to be allowed access.

?

Bureau's vast network of databases enable detection of malicious behaviour like identity theft, account takeover that effectively counter fraud.

Here's how one India's largest insurers minimised fraud

Summing up

Digital payments have grown phenomenally in volume and popularity, and with a constant thrust from the RBI, digital and financial literacy has accelerated exponentially. The core theme of the vision document is 'E-Payments for Everyone, Everywhere, Every time' (4Es)'. At Bureau, we are working towards ushering in a new era of frictionless and fraud-free transactions that will deliver unprecedented trust and security to businesses and consumers alike. To know more, click here

?

A well-functioning payment system can aid in economic growth and promote financial inclusion. The need for such a system is accentuated in a developing country like India, where the JAM (Jan Dhan, Aadhaar and Mobile) trinity and low-cost mobile and data penetration have played a critical role in boosting the adoption of digital payments in the country. The UPI-enabled transactions in June 2022 were 5.86 billion in number and the transaction value exceeded Rs 10 lakh crores, registering an year-on-year growth of 108% and 85% respectively.

?

What is outlined in the Payments Vision 2025' document?

In its 'Payments Vision 2025' document, the Reserve Bank envisions a three-fold jump in digital payments and aims to establish India as a powerhouse of payments globally. The apex bank wants to make this rise in digital banking an irreversible shift without compromising the integrity of payment systems. It aims to improve the payment systems' reach, security, customer confidence and convenience.

?

As noted in the Vision document, India has one of the most modern payment systems in the world. The recent Phonepe-BCG report on digital payments expects the size to triple from US$3 trillion today to US$10 trillion by 2026.

?

With an enabling regulatory infrastructure and more significant usage of smartphones and mobile data, India witnessed an increase in the adoption of digital payments. And the Covid19 pandemic further accelerated the shift toward digital payments.

?

The 'Vision 2025' document is anchored on the five pillars – Integrity, Inclusion, Innovation, Institutionalisation and Internationalisation. Through these, the RBI intends to achieve ten outcomes, including growth of UPI at more than 50%, increase in PPI transactions by 150%, and the growth of registered customer base for mobile-based transactions by more than 50% per annum, among others.

Five pillars of Payment Vision 2025

Integrity

The integrity of payment systems is critical in strengthening customer confidence. To enhance the integrity of the payment systems, specific initiatives like the exploration of alternate risk-based authentication mechanisms, an 'Online Dispute Resolution' system for fraud monitoring and reporting and ring-fencing of domestic payment systems like the need to mandate domestic processing of payment transactions are envisaged.

?

Inclusion

The digital payment penetration in India exhibits a skewed pattern, with Tier III-VI cities having a lower penetration due to a lack of tech-savviness and an insufficient number of touchpoints. Recent initiatives like UPI123PAY (UPI payments for feature phone users) are expected to provide a fillip to the inclusion efforts. In addition, initiatives like a framework for geo-tagging of payment system touchpoints, review of guidelines on Prepaid Instruments (PPIs), and customer awareness activities are envisaged to deepen the access and usage of payment systems.

?

Innovation

Innovation in payment systems is needed to make payments more convenient and safe. The recent initiatives by RBI like opening up UPI for credit cards and organising hackathons like 'HARBINGER 2021 – Innovation for Transformation', aim to encourage innovation in the digital payment space. On the anvil are initiatives like reviewing the need for multiple payment identifiers (doing away with Indian Financial System Code (ISFC)) for fund transfers and IoT-based payments. The RBI is also expected to issue guidelines on payments involving BNPL soon.

?

Institutionalisation

The Payment and Settlements Act 2007, which governs the payment systems, would be reviewed according to the fast-changing payments landscape.

?

Internationalisation

RBI would support the expansion of UPI to countries across the world. Further, the widely anticipated launch of the Central Bank Digital Currency (CBDC) is expected to usher in greater efficiencies in domestic and cross-border payments and settlements.

To know more about CBDC, read Artificial Intelligence in CBDC.

?

How Bureau shares the vision

With the significant rise in digital payments in the last few years, the threat and fraud landscape has grown by leaps and bounds.

?

Every month, frauds worth more than Rs 200 crore are committed through UPI alone. Rising frauds, a lack of robust infrastructure to detect or prevent such instances, and the absence of a redressal mechanism are some of the concerns plaguing online digital payments. Moreover, fraudsters are becoming more sophisticated daily, using methods such as vishing, SIM cloning/swapping, malicious QR codes and apps, and more. Ironically, bad actors leverage the same technologies developed to build better consumer solutions.

?

Fortunately, there is also good news. New technologies are constantly emerging to keep us ahead of fraudsters. Bureau as an identity orchestration platform has been powering businesses to authenticate users and prevent fraud without adding friction to the customer's journey. Thus, Bureau's vision perfectly resonates with that of the RBI.

?

At Bureau, we believe fraud can be fought without increasing friction and sacrificing customer experience on the altar of risk.

?

Bureau is particularly seized by the problem of integrity in the digital world and the inadequacy of the current systems like SMS OTP. Bureau's One Tap Login (OTL) enables frictionless login that securely verifies mobile numbers leading to a sleek customer experience.

?

Bureau's onboarding platform works seamlessly and efficiently to verify KYC and comply with regulatory guidelines, including AML.

RBI’s vision of exploring alternate risk-based mechanisms like behavioural biometrics and location of the user for authentication is in sync with Bureau’s solution to reduce fraud. Bureau’s risk-based authentication uses risk scores based on rules that analyse various factors such as device, IP, phone number, and email id to determine if a user is to be allowed access.

?

Bureau's vast network of databases enable detection of malicious behaviour like identity theft, account takeover that effectively counter fraud.

Here's how one India's largest insurers minimised fraud

Summing up

Digital payments have grown phenomenally in volume and popularity, and with a constant thrust from the RBI, digital and financial literacy has accelerated exponentially. The core theme of the vision document is 'E-Payments for Everyone, Everywhere, Every time' (4Es)'. At Bureau, we are working towards ushering in a new era of frictionless and fraud-free transactions that will deliver unprecedented trust and security to businesses and consumers alike. To know more, click here

?

TABLE OF CONTENTS

See More

Recommended Blogs

Why Financial Crime Prevention's Future Is Collaborative

Across the UK and European Union, fraud is being reshaped by forces beyond traditional controls. Real-time payments compress decisions, digital onboarding.

How Middle East Banks Can Rethink Fraud Prevention

Rapid digital adoption is reshaping banking across the Middle East. Instant onboarding, digital wallets, and super apps are now the norm, expanding the attack.

Building Real-time Defenses in an Always-on Economy

In an always-on, connected economy, risks are created in real-time, rather than at discrete checkpoints. Defense strategies must, accordingly, level up to.

TABLE OF CONTENTS

See Less

Landing Page.

Simple, bold.

Sign Up

Download

Solutions

Resources

© 2026 Bureau . All rights reserved.

Solutions

Industries

Resources

Company

Solutions

Industries

Resources

Company

© 2026 Bureau . All rights reserved.

Follow Us

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

Leave behind fragmented tools. Stop fraud rings, cut false declines, and deliver secure digital journeys at scale

Our Presence

© 2026 Bureau . All rights reserved.